Introduction

The Insolvency and Bankruptcy Code (‘IBC’), enacted in India in 2016, provides a comprehensive framework for resolving insolvency cases. Given the unique challenges that Micro, Small, and Medium Enterprises (‘MSMEs’) face during financial distress, the IBC includes specific provisions tailored for their insolvency resolution. MSMEs are the backbone of the Indian economy, playing a pivotal role in employment, production, economic growth, entrepreneurship, and financial inclusion. The MSME sector supports the livelihoods of nearly 110 million people and contributes 30% of India’s GDP[i]. This article explores the complexities of the insolvency resolution process for MSMEs under the IBC, examines the challenges within the MSME-specific framework, and highlights key sections of the IBC, international practices, and their importance in enhancing the resolution process for this vital sector of the economy.

Objective behind introducing provisions for MSME under IBC

Introducing specific provisions for MSMEs within the IBC aims to create a balanced and supportive environment for MSMEs, acknowledging their critical role in the economy and providing mechanisms to help them navigate financial difficulties effectively. The key objectives include:

Recognizing the critical importance of MSMEs. MSMEs play a vital role in India's economic landscape by contributing significantly to the gross domestic product and creating substantial employment opportunities. Their dynamic presence is crucial for fostering economic growth, innovation, and diversification.

Due to their distinct business models and simpler corporate structures, MSMEs encounter unique insolvency challenges. Therefore, it was essential to develop targeted strategies to address these challenges efficiently. This includes understanding the specific needs of MSMEs during financial distress and creating tailored solutions that reflect their operational realities and complexities.

Accelerate the insolvency resolution process to ensure timely resolution for MSMEs. This involves reducing delays, optimizing procedural timelines, and implementing fast-track mechanisms. Quicker outcomes will enable faster recovery for MSMEs, reducing the financial strain associated with prolonged insolvency proceedings.

The insolvency resolution process is designed to be cost-effective, reducing the financial burden on MSMEs. A cost-effective approach helps ensure that MSMEs retain more of their resources and can focus on recovery and growth.

Maximizing value for all stakeholders, including creditors, employees, and shareholders. Ensuring fair and equitable treatment of all parties will help build trust and facilitate smoother resolution proceedings.

6. Minimize disruption to MSME operations during insolvency resolution by allowing continued activities, ensuring access to necessary resources, and maintaining operational stability to preserve market position and viability.

Preserving jobs throughout the insolvency resolution process is a key objective, as strategies should be implemented to protect employment and support the workforce. This includes restructuring plans that aim to retain jobs and provide support to employees affected by the insolvency.

Definition of MSMEs

In accordance with the provision of Micro, Small & Medium Enterprises Development

Act, 2006 (‘MSMED’) MSMEs are classified as below:

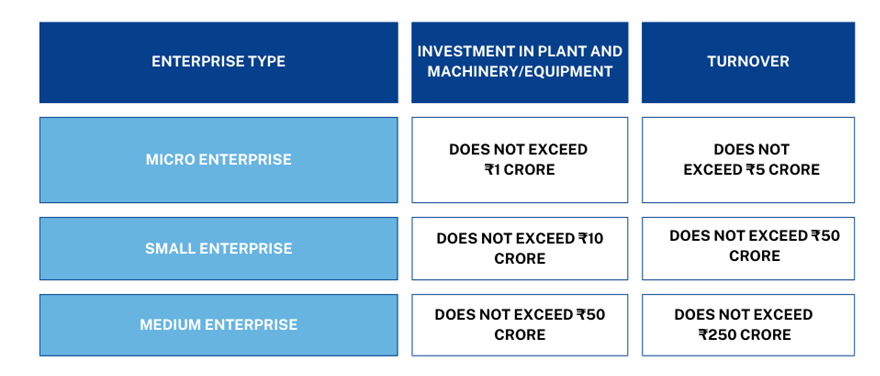

(i) a micro enterprise, where the investment in plant and machinery or equipment does not exceed one crore rupees and turnover does not exceed Rs. 5 crores;

(ii) a small enterprise where the investment in plant and machinery or equipment does not exceed ten crore rupees, and turnover does not exceed Rs. 50 crores, and

(iii) a medium enterprise, where the investment in plant and machinery or equipment does not exceed fifty crore rupees, and turnover does not exceed Rs. 250 crores.

MSMED Act, 2006

The MSMED Act, enacted in 2006, addresses policy issues and investment ceilings for MSMEs, aiming to develop these enterprises and enhance their competitiveness. It provides a legal framework for recognizing manufacturing and service entities, defining medium enterprises, and integrating micro, small, and medium tiers. The MSMED Act establishes a national consultative mechanism with balanced stakeholder representation and advisory functions. Key features include funds for MSME promotion, development programs, progressive credit policies, preferential government procurement, and mechanisms for addressing delayed payments and business closures. However, the effectiveness of resolving payment delays through the facilitation council has been limited due to issues with enforceability.

Background behind introducing the IBC (Amendment) Ordinance 2021

In light of the widespread impact of the COVID-19 pandemic on global businesses, financial markets, and economies, including micro, small, and medium enterprises in India, the President of India in the seventy-second year of the Republic of India promulgated an ordinance to amend the IBC. Recognizing the severe financial distress caused by the pandemic, the government implemented measures to support affected businesses, including raising the minimum default amount required to initiate corporate insolvency resolution processes (‘CIRPs’) to Rs. 1 crore and suspending the initiation of such processes for defaults occurring during the year starting from 25.03.2020. This suspension ended on 24.03.2021.

The IBC (Amendment) Ordinance 2021

The IBC (Amendment) Bill 2021 was introduced in Lok Sabha on 26.07.2021 and was promulgated on 04.04.2021. The IBC addresses insolvency, a situation where individuals or companies cannot repay their outstanding debt. It provides a time-bound process for resolving corporate debtor (‘CD’) insolvency called the CIRP, which must be completed within 330 days. The debtor or creditors can initiate CIRP for defaults of at least Rs. 1,00,000, with a committee of creditors (‘CoC’) deciding on the resolution plan, which may involve debt payoff through merger, acquisition, or restructuring. If no resolution plan (‘Plan’) is approved within the specified time, the company is liquidated, and a resolution professional (‘RP’) manages the company's affairs during CIRP. The Bill also introduces the pre-packaged insolvency resolution process (‘PPIRP’) for MSMEs, which can only be initiated by debtors who must have a base Plan ready, with the debtor retaining management of the company during PPIRP.

S. 29A of the IBC

The IBC (Second Amendment) Act, 2018 ('Second Amendment') has provided significant relief to MSMEs by relaxing the stringent provisions of s. 29A of the IBC. This section sets forth eligibility criteria for resolution applicants, which is crucial for submitting a Plan. The Second Amendment introduced s. 240A of the IBC, exempting MSMEs from the restrictive clauses of ss. 29A(c) and 29A(h) of the IBC when submitting a Plan. This prevents a promoter from being classified as a wilful defaulter or disqualified under s. 29A of the IBC, to bid for the MSME's Plan. Moreover, the Second Amendment empowers the central government (‘CG’) to grant further exemptions or modifications in the public interest, aiming to facilitate MSMEs in securing bidders and avoiding liquidation.

In a recent judgment in Hari Babu Thota v. Shree Aashraya Infra-Con Ltd.[ii], the Hon'ble Supreme Court of India (‘SC’) affirmed the exemptions from disqualifications under s. 29A of the IBC applies even if the CD attains MSME status after initiating the CIRP.

In the case of K. Satheesh Babu Rajesh v. Mr. George Varkey[iii], the Kochi Bench of the National Company Law Tribunal (‘NCLT’) clarified that a promoter of an MSME CD is eligible to submit an expression of interest or Resolution Plan in their individual capacity. This order reaffirms s. 240A of the IBC, specifying that the disqualifications under ss. 29A(c) and 29A(h) of the IBC do not apply to MSME insolvencies. Thus, the law is settled regarding the eligibility of resolution applicants to propose plans during MSME insolvencies.

PPIRP

The IBC Amendment Act 2021 was notified by the CG on 12.08.2021, and PPIRP was introduced.

Eligibility for PPIRP: An application for the PPIRP can be made in the event of a default of at least one lakh rupees. The CG may increase this minimum default level to one crore rupees through a notification.

Chapter III-A: The IBC (Amendment) Ordinance 2021 amends the IBC to add ch. III-A to address PPIRP. A corporate applicant can lodge an application to start PPIRP with the adjudicating authority concerning an MSME CD, subject to specific conditions as mentioned in s. 54A of the IBC.

PPIRP & MSME

In this mechanism, the CD’s assets are negotiated before filing an application under ss. 7, 9, and 10 of the IBC. Once the negotiations conclude, the CoCs and the NCLT must approve the proposed plan. The PPIRP for MSMEs will be subject to s. 14 of the IBC, which enforces a moratorium from the start through the end of the process. Unlike traditional CIRP, the current promoters and management of the CD retain control during the PPIRP. If the existing management's base Plan is not approved or does not allow full payment of proven claims, the RP will invite other applicants to submit competing plans. S. 61(3) of the IBC allows for an appeal against the ruling approving the pre-pack resolution process.

Stages of PPIRP

The pre-packing procedure can be divided into three stages:

Stage 1- The CD submits a base Plan for consideration by a CoC.

Stage 2- If the base Plan fails, the RP invites other applicants to submit competing plans, which are then examined by the CoC.

Stage 3- The base plan and the invited plans are compared, and the best plan can be enhanced based on input from the others.

The law mandates that the process must be completed within 120 days from admission, divided into two parts: (i) 90 days for the CoC to approve the Plan and (ii)30 days for adjudication by the adjudicating body. If no Plan is adopted within 90 days, the RP must file an application to end the pre-pack procedure.

Interplay with Sustainable Development Goal (SDG-8)

Economic growth, a key goal under SDG 8[iv], is the foundation for introducing the new IBC Ordinance, which has positively transformed the country's insolvency regime. The ordinance aligns with SDG-8, which aims to ensure higher productivity through technological innovation and policies that encourage job creation and entrepreneurship. This change helps protect MSMEs, which provide jobs for many skilled and unskilled workers, from threats posed by economic conditions. By implementing SDG-8, the legislature aims to prevent job reduction due to natural calamities, thus ensuring economic prosperity and development for the lower strata of society. The PPIRP will help MSMEs recover from financial distress and prevent job losses due to natural calamities, thereby ensuring economic prosperity and the development of the lower strata of society.

Differences between PPIRP and CIRP

The most significant feature of a PPIRP is that, unlike the CIRP, it allows the promoters or directors of the defaulting business to remain in control. CIRP allows the RP to control the business in consultation with the financial creditor (‘FC’). As per s. 7 of the IBC, CIRP can be initiated by the CD, FC, or operational creditor, but a PPIRP can only be initiated by the CD. This makes PPIRP cost-effective and less time-consuming for MSMEs compared to CIRP. The PPIRP must be completed within 120 days, with 90 days for submitting the Plan and 30 days for the NCLT approval. In contrast, the time frame for completing the CIRP is 330 days. This reduced timeframe alleviates the burden on the NCLT and NCLAT.

Any CD designated as a micro, small, or medium company under s. 7(1) of the MSMED, and any defaulter under s. 4 of the IBC can begin the PPIRP procedure, subject to the following conditions[v]:

A CD that has not completed a PPIRP or CIRP within three years of the commencement date.

Such a CD that is not going through the CIRP procedure.

There is no liquidation order against such a CD under s. 33 of the IBC.

It is qualified to submit a Plan under s. 29A of the IBC, subject to s. 240A of the IBC.

If the FCs are not related to it and represent not less than 66 percent of the financial debt's value, they have accepted the proposal of an insolvency professional being appointed RP for conducting the PPIRP.

There is a declaration made by the majority of the directors or partners of the CD, stating inter-alia:

a. The CD, within a period of 90 days, will file for initiating the PPIRP;

b. The PPIRP will not be initiated to defraud any person;

c. The approved RP’s name;

7. At least three-fourths of the CD’s total partners have passed a special resolution approving the filing of an application initiating the PPIRP.

The AA will be required to either accept or reject an application for PPIRP within 14 days of receipt. If the application is accepted, the CoC must accept the Plan and be approved with 66% of voting shares within 90 days. If the Plan is not approved, the PPIRP will be terminated, resulting in liquidation and distribution of assets to the creditors.

International Practices

International practices in insolvency proceedings vary significantly across jurisdictions, showcasing diverse approaches to corporate reorganization and debt management:

United States

In the US, businesses and individuals seeking relief under the US Bankruptcy Code can file a petition under chs. 7, 9, 11, 12, 13, and 15[vi]. The US Bankruptcy Code specifies ‘small business debtors’ but does not explicitly refer to MSMEs or SMEs. Ch. 11 bankruptcy involves the reorganization of a debtor’s debts and assets and is available to individuals, sole proprietorships, partnerships, and corporations. The primary purpose of filing for ch. 11 bankruptcy is to prevent a business from permanently closing, provided the company's financial situation makes debt restructuring a viable option.

United Kingdom

The UK employs the concept of 'phoenixing,' allowing promoters of bankrupt companies to bid for their assets without assuming previous debts[vii]. Directors and employees of insolvent companies can establish new firms, provided they are not personally bankrupt or disqualified from managing a company. Legal mechanisms like company voluntary arrangements (CVAs) and individual voluntary arrangements (IVAs) offer structured repayment plans outside bankruptcy, overseen by courts.

Republic of Korea

The Debtor Rehabilitation and Bankruptcy Act (‘DRBA’) consolidated the Corporate Reorganisation Act, 1962, the Composition Act, 1962, and the Bankruptcy Act, 1962, to streamline bankruptcy and rehabilitation procedures for insolvent companies[viii]. Applicable to all types of legal entities, including individuals, corporations, and unincorporated foundations or associations, the DRBA includes rehabilitation procedures for corporates and individuals, streamlined Summary Rehabilitation Procedures (SRP) for SMEs, rehabilitation procedures for individuals with small debts, and liquidation procedures for individuals and corporates, including a summary liquidation procedure for SMEs.[ix]

Canada

Canada's Bankruptcy and Insolvency Act includes provisions for division II proposals, a streamlined mechanism for small businesses and sole proprietors. These proposals enable debtors to negotiate repayment plans with creditors, providing an efficient alternative to bankruptcy while ensuring creditor protection. Bankruptcy provides individuals, including business sole proprietors, with a chance for a fresh financial start. First-time bankrupts may receive an automatic discharge after filing for bankruptcy or being declared bankrupt, which occurs either in nine months or 21 months, depending on whether they have surplus income. A creditor, the trustee, or the superintendent of bankruptcy can contest this discharge[x].

Australia

Australia offers debt agreements under the Bankruptcy Act, allowing debtors to propose binding repayment arrangements to creditors. This alternative to bankruptcy helps debtors avoid severe financial consequences while meeting their obligations through structured payments overseen by the official receiver. Debt agreements were established as an alternative to bankruptcy, designed to offer debtors a cost-effective way to negotiate arrangements with their creditors while avoiding the more severe consequences of bankruptcy. These binding agreements, outlined in part IX of the Bankruptcy Act, 1966, allow insolvent debtors to propose legally binding repayment plans to their creditors. Once creditors accept the proposal, the debtor is released from the associated debts upon completing the agreed-upon payments.[xi]

These international practices highlight varying legal frameworks and procedural innovations to support economic resilience and debt restructuring across different scales of enterprises and jurisdictions. Each system reflects nuanced approaches to balancing creditor rights, debtor rehabilitation, and economic stability.

Conclusion

The PPIRP is a novel concept introduced in India, inspired by successful implementations in countries like France, the United Kingdom, the United States, the Netherlands, and Germany. This mechanism offers a fast, cost-effective alternative to traditional CIRP, particularly benefiting MSMEs. Effective implementation requires insolvency professionals to discharge their duties independently, with regular monitoring and adherence to high professional standards set by the Insolvency and Bankruptcy Board of India (IBBI). While the scheme presents significant advantages, such as efficient resolution of distressed companies and cost savings, it also faces challenges. Critics argue that the typically smaller loan amounts in MSMEs may limit the scheme's impact. Despite these challenges, the introduction of PPIRP adds a new dimension to India's bankruptcy proceedings. There is a growing demand from the industry to extend this scheme to larger businesses, but any such expansion will require careful evaluation to address potential issues and ensure its success.

End Notes

[i] Annual Report, 2020-21, Ministry of Micro, Small and Medium Enterprises, Government of India

[ii] Civil Appeal No. 4422/2023

[iii] (2021) ibclaw.in 61 NCLT

[iv] Innoventive Industries Ltd. v. ICICI Bank [2017] 82 taxmann.com 190/139 CLA 335/142 SCL 11/205 Comp Case 23 (NCLAT)/2017 SCC OnLine NCLT 13607

[v] The Insolvency and Bankruptcy Code (Amended), 2021 § 54A

[vi] US Bankruptcy Code-Title 11 of the United States Code, Corporate Finance Institute.

[vii] https://www.gov.uk/government/publications/phoenix-companies-and-the-role-of-the-insolvency-service/phoenix-companies-and-the-role-of-the-insolvency-service

[viii] https://www.allenovery.com/global/-/media/allenovery/2_documents/practices/restructuring/restructuring_across_borders/18_korea.pdf

[ix] “Republic of Korea: Financial Sector Assessment Program-Technical Note-Insolvency and Creditor Rights,” International Monetary Fund.

[x] “Micro, Small and Medium Enterprises (MSME) insolvency in Canada,” Allard Research Commons.

[xi] https://www.sl.nsw.gov.au/find-legal-answers/books-online/dealing-debt-legal-guide-personal-debt-nsw/bankruptcy-and-debt

Authored by Pratima Ajmera, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinion.